With this update, this will be the last one of these in this series with this structure. The combination of premium increases and subtle changes in the product structure choices being made as a result means future comparisons need to be tweaked enough to be different.

I have been discussing managing medical premiums for quite some time. This article I wrote in 2016 is the start where I discuss the life cycle of medical insurance for the typical household. This discussion and approach is still quite valid.

However, with Covid, challenges with the public medical system and cost-of-living pressures, medical insurance remains an essential tool to ensure you have access to the medical care you need, but it's a whole lot more expensive than it used to be.

I provided updates to the original 2016 article in 2023 and again in 2024, as increased pressure on premiums began to take effect. 2024 marked the beginning of a rough ride for medical premium hikes, a trend that has continued throughout 2025.

2025 kicked off with 4 out of 5 insurers announcing premium increases. The range of increases experienced against last year has been 15 to 40% plus age-related increases, with July seeing year-on-year double-digit increases against 2024.

The premium increases notified aren't just the increase you see; there are normal age-related increases on top of this, as you're a year older and you have slightly more risk of issues developing. The younger age group is 1-2% for being a year older and 5-10% for those middle-aged and older. It might not sound like a big deal, but compound that over your lifetime, and you get $40 monthly premiums in your teens that become $700 per month by age 70.

That might scare you a bit, and what you don't know about the public health system means that you're probably over-reliant on the expectation it will provide.

This link for Public Health services delivery response is an interesting one. It stopped being updated when the election rolled around in 2023, but it has since restarted. However, suddenly, what was red isn't, which makes things look better than they actually are.

How might they have achieved this:

- Plain old increased barriers to accessing care.

- The pressure on GPs to manage conditions at the GP level results in fewer referrals to public specialists. Our clients are telling us that wait times for specialists are long, and it's taking some effort to get GPs to refer publicly.

- Medical insurance is not a problem; GPs happily refer patients privately for treatment. You get the care you need, and they remove some of their ongoing management workload, trying to game the public system to look after people.

- Since my update here in March 2025, it seems GPs have moved from referring you into the public system and not asking about insurance to actively questioning if a patient has cover and then referring them privately if they have insurance.

My continued message is you need Medical Insurance and to regularly review your coverage to meet your changing needs

The reality is that the type and structure of your medical policy will change throughout your life, as different stages require different approaches.

When considering medical insurance, you're often basing decisions on the assumption that this policy will remain unchanged for 40-plus years, which is blatantly unrealistic. But people decide on and operate their policies in this way.

The point of this update is to raise the flag that restructuring medical coverage that is getting expensive is possible, and a reduced, affordable level of coverage is far better than throwing it all away.

What will surprise you is I can provide coverage for a 75-year-old couple with a similar premium to a 30-year-old couple with kids. It is a matter of structure and alignment with available resources, but it is possible.

Writing this update mid-October, we have:

- Increased premiums are coming for those at AIA, this time, age-banded rather than flat increases. Showing that certain ages are where a lot of claims are coming from, and the older clients aren't claiming quite as much. Less of and an increase for those retired, but a reasonable bump for those under 40. 17-25% base increases from 1 November.

- Southern Cross have announced new rates in November, which look to be about 3% on July 2025's rates and like AIA, the July 2025 review was age-banded, 14-27% year on year, July 2024 to July 2025.

- Partners Life has moved to quarterly rather than annual premium reviews, with July picking up 2.3% on April 2025 for an annual increase of 22-23%

- nib has come to market on all of their non-guaranteed policies, adding a 20% co-payment for specialists and diagnostic testing and removing some minor benefits. The biggest loss here is the cover in Australia for those relying on this working for them after moving to Australia.

Let's get started:

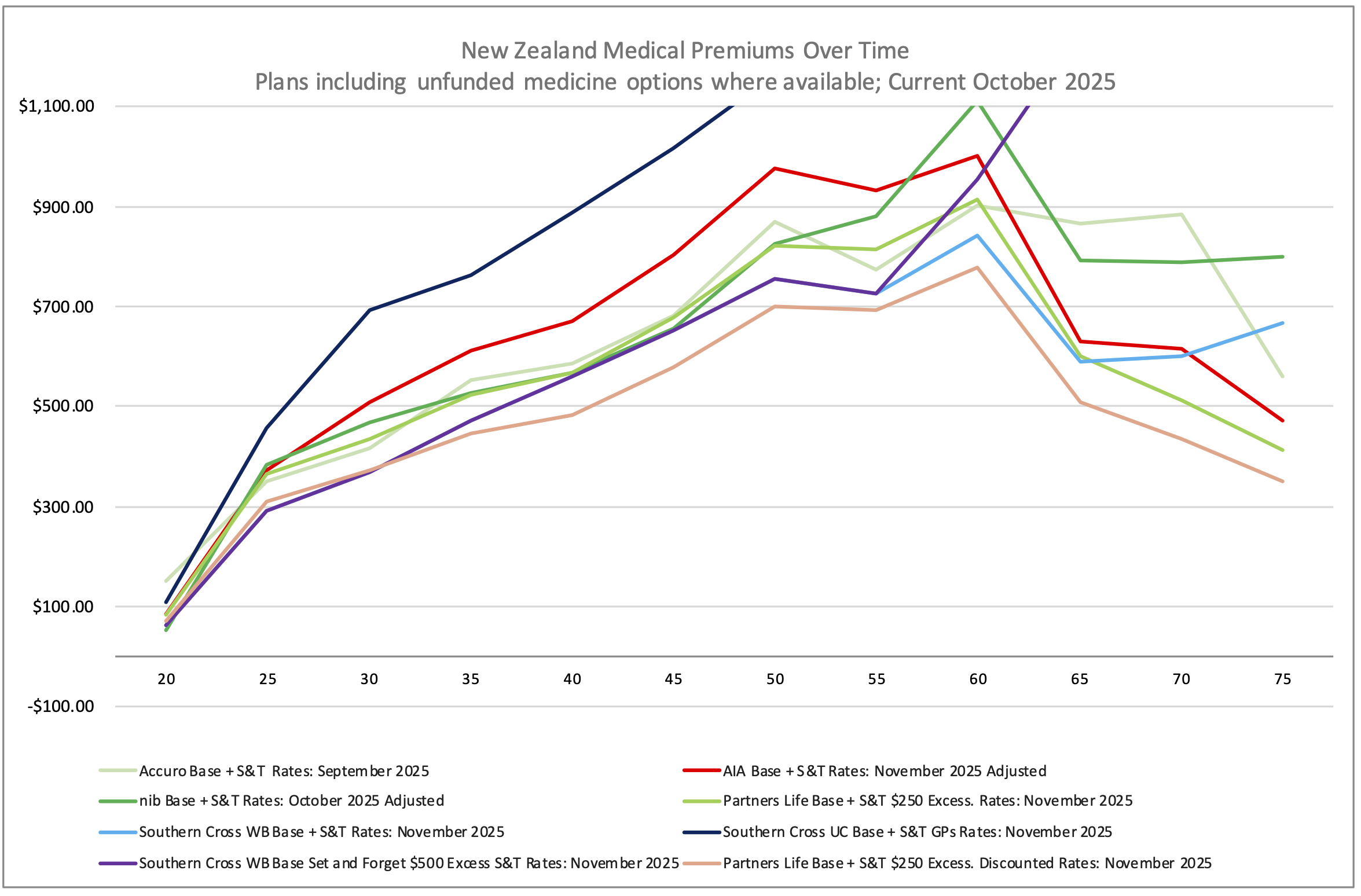

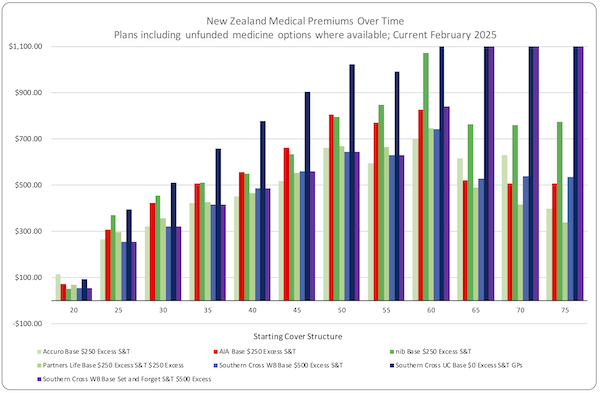

The chart below outlines what I'm going to step you through. As you can see, it remains pretty tight until around 50, then it spreads, and once you approach retirement, it gets a bit squiggly. Interestingly, when compared to 2016, there was significantly more variation in premiums between 25 and 50.

The clear message is that UltraCare offers many benefits, particularly for pre-existing condition qualification. However, you should consider transitioning to Wellbeing plans as soon as possible. This is a key point where consulting with us is advisable, as we can restructure your cover to preserve your pre-existing condition coverage.

- Also, UltraCare is the only product used here that includes GP and prescription costs, so it is expected to be more expensive than the average. However, the premium increase after age 55 is astoundingly dramatic, and anyone over age 55 with it needs to seek advice now!

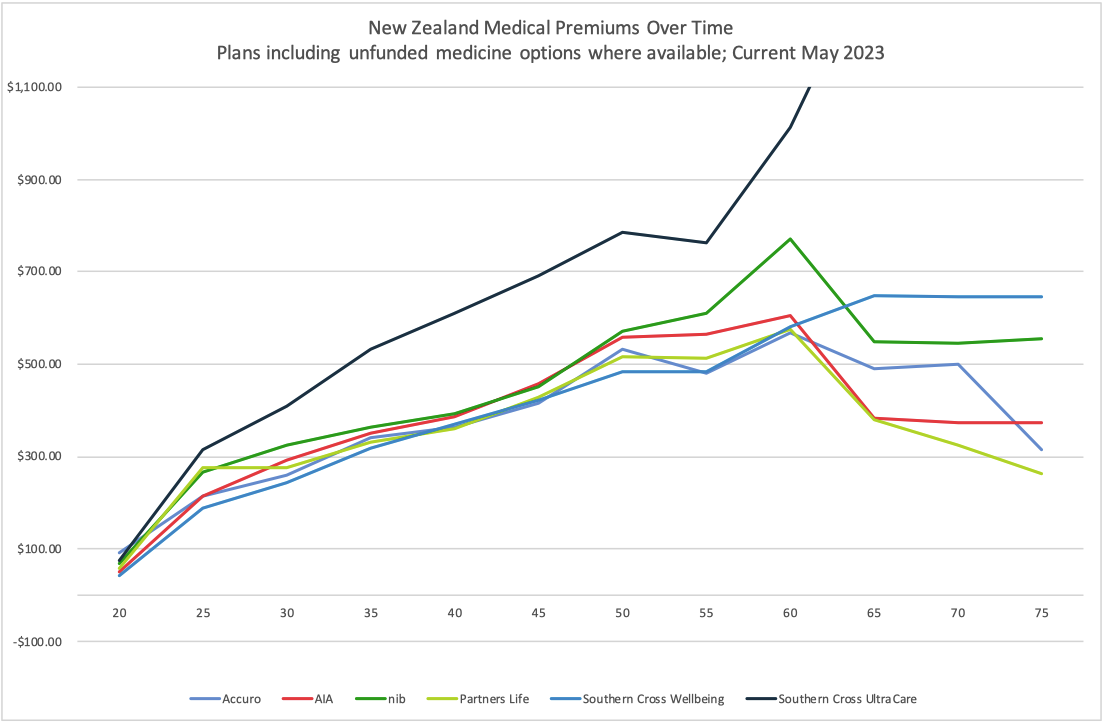

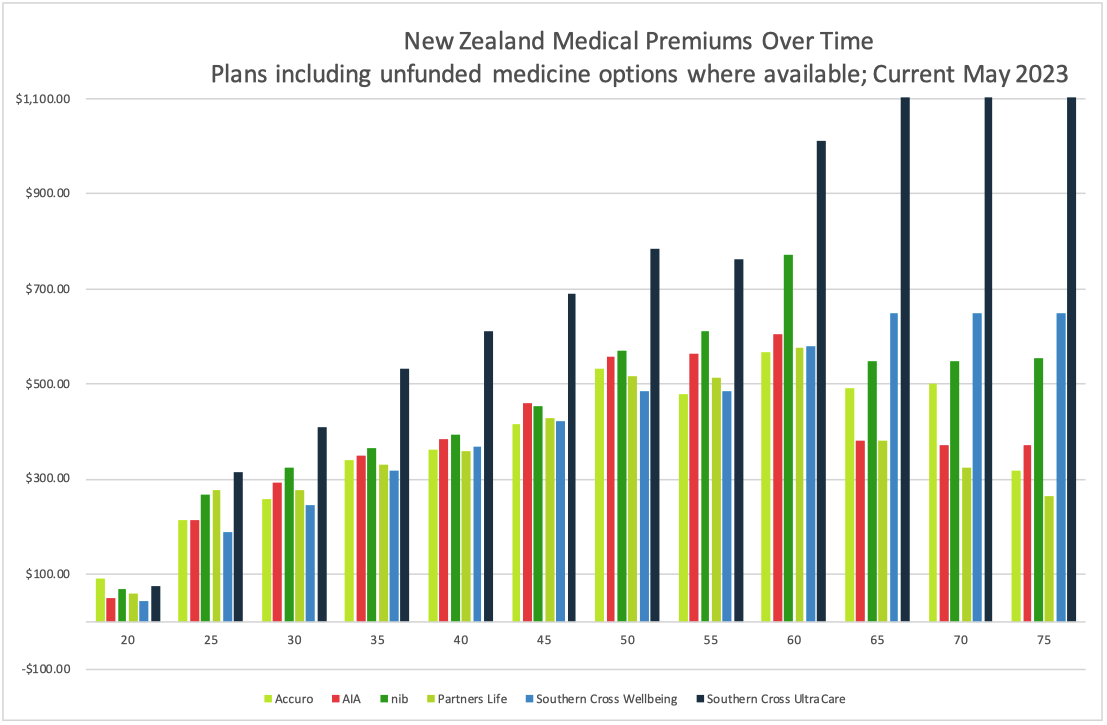

This is the picture from May 2023

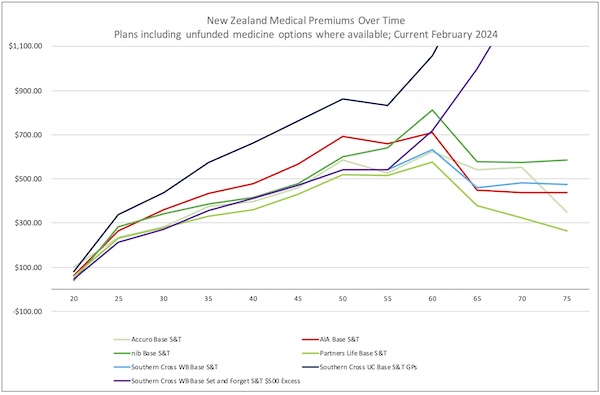

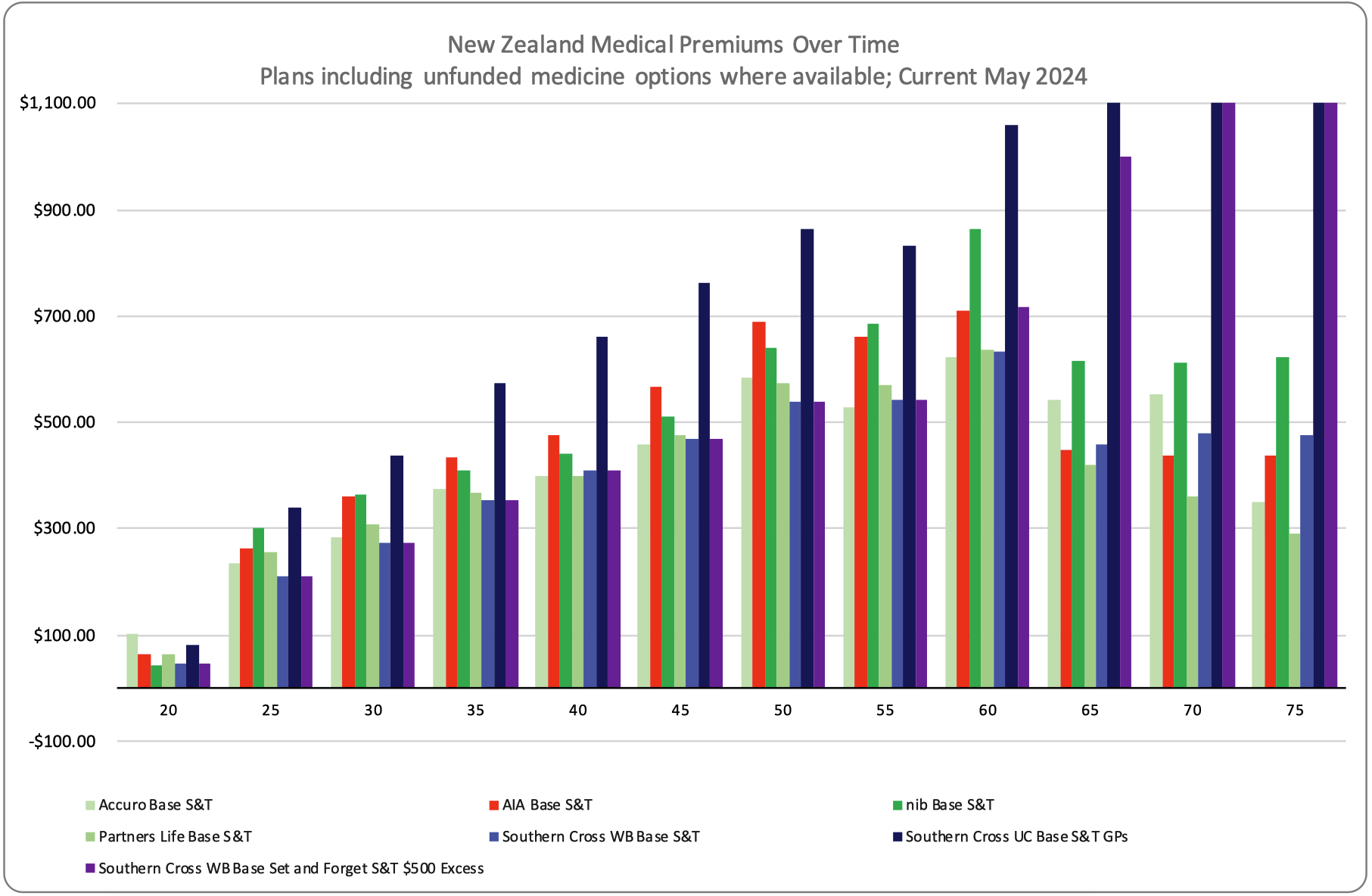

This is the picture 12 months later in May 2024

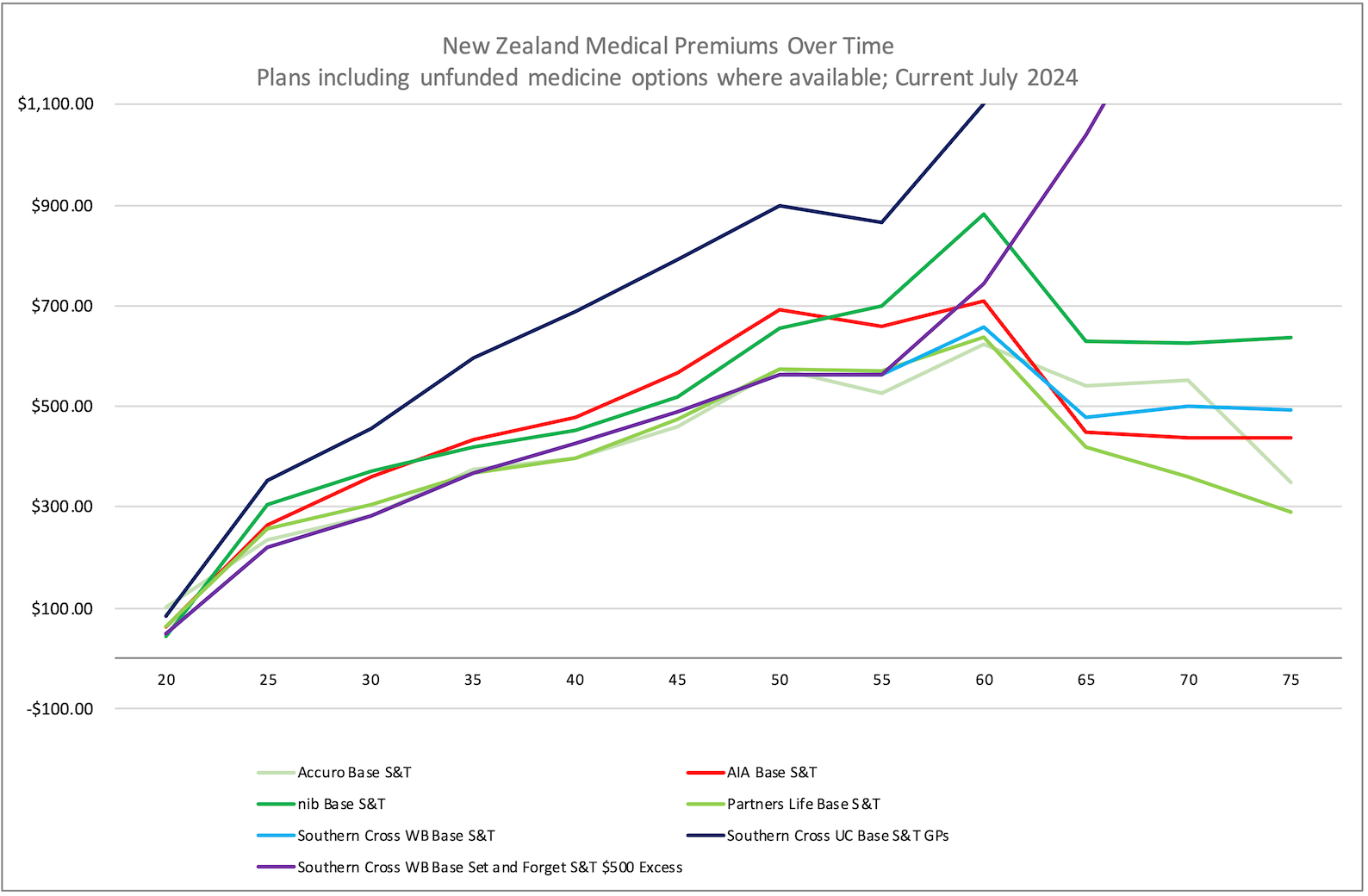

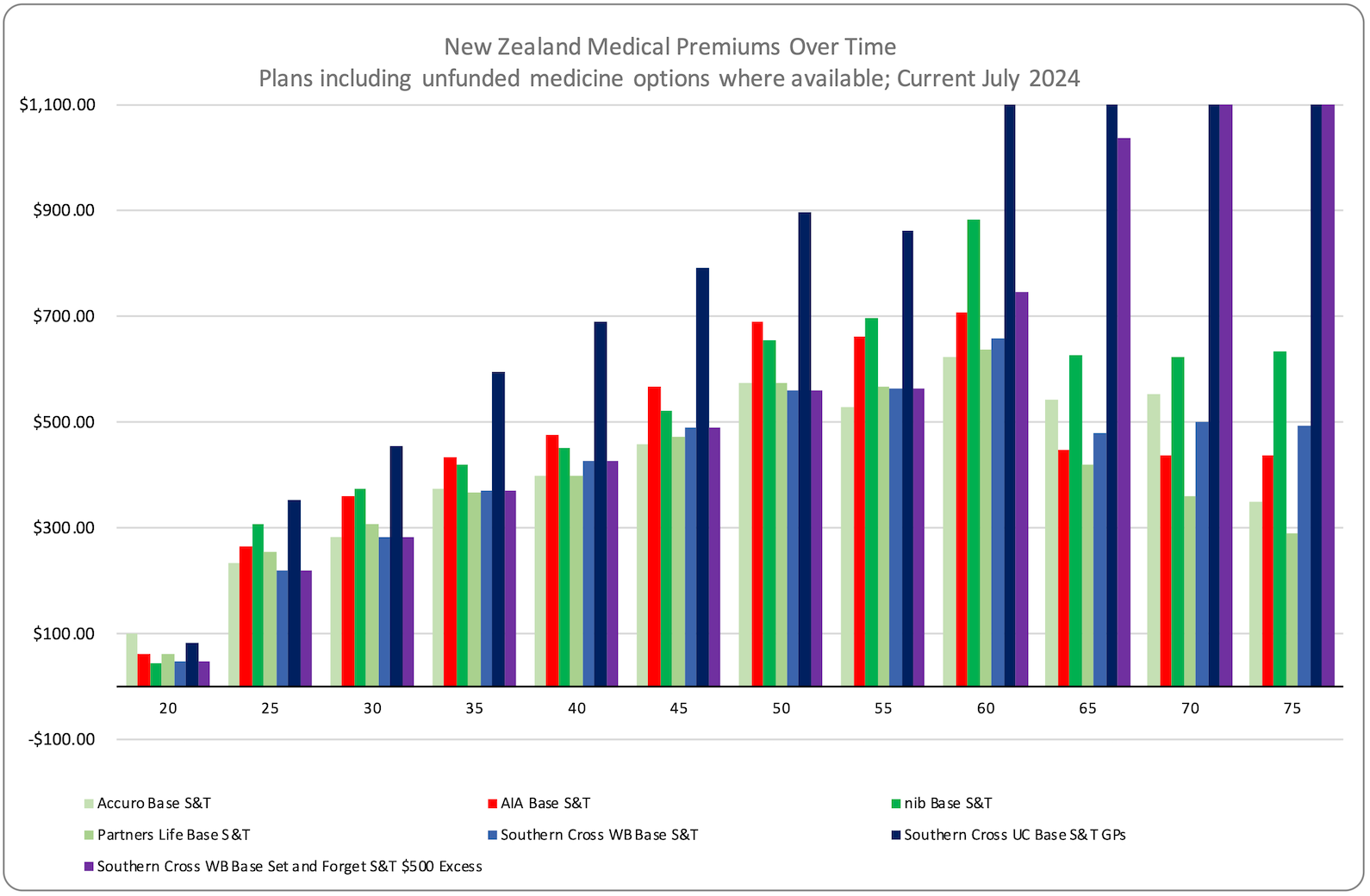

And this is the picture from July 2024.

7 months later, the picture is quite different. (nib rates July 2024, AIA rates November 2023)

And coming up the end of 2025 (with some corrected rate updates for AIA & nib)

This last one has Partners Life's multi-benefit discount added, effective from 1 November 2025.

The premium is accurate at the time of publishing, based on standard premium rates, and subject to a medical assessment. Some providers have additional plans available; the most equivalent plans have been used for comparison purposes. The Southern Cross premiums illustrated do not have the unfunded medicines option added and are an additional premium to this illustration.

Please refer to my prior article for the life cycle story these charts discuss:

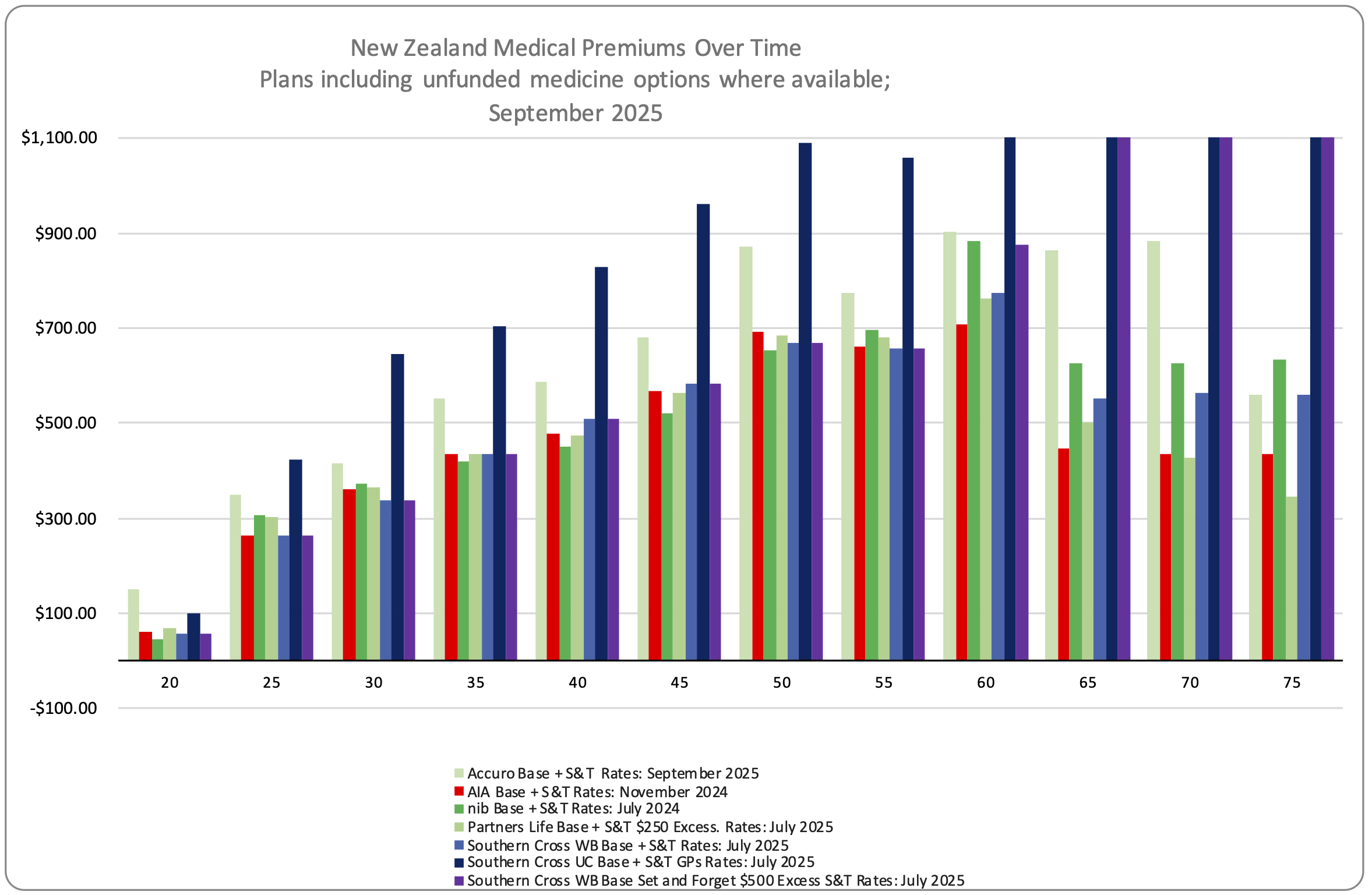

The graph below covers the same information as above, giving a better view of what each provider is doing at a particular age.

This is the picture from May 2023

This is the picture 12 months later, in May 2024

And this is the picture from July 2024.

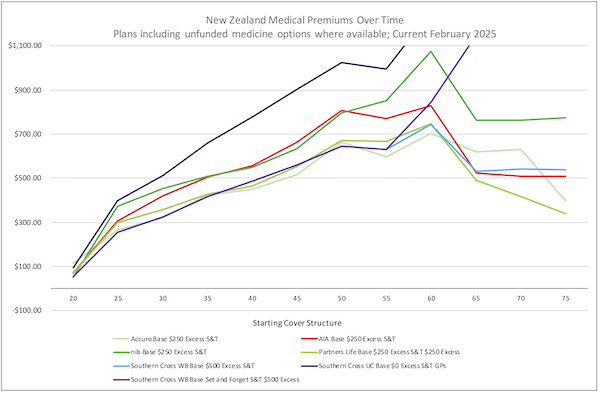

and the February 2025 picture.

Premium is accurate at the time of publishing, based on standard premium rates and subject to a medical assessment. Some providers have additional plans available; the most equivalent plans have been used for comparison purposes. The Southern Cross premiums illustrated do not have the unfunded medicines option added and are an additional premium to this illustration.

Summary:

Looking across all providers and all ages for this sort of typical scenario, the average premium is $579 per month, including UltraCare and $484 per month without UltraCare in the mix. Some providers will be consistently positioned, and some will be across the spectrum as age and policy structure have a bigger impact than with other providers.

The average cost of coverage has moved significantly in the last ten years. At the same time, average earnings have increased, and people have adapted to the increased costs of living.

- This is an outline of a typical medical insurance strategy and one that plays out every day.

- This isn't my advice at work; these are the decisions clients make once they have the information to make an informed decision, decisions that affect them.

- Being able to discuss the options means you retain valuable benefits that you may have otherwise cancelled due to a lack of alternative options.

I’ve seen people with very few claims, as well as others who have had multiple claims and had thousands paid.

- For example, a couple of knees and a bypass, $85,000 within three years,

- and cancer surgery and treatment, $180,000.

Sometimes, it's nothing for years and years, then bang, it's a run of significant claims. Other times, it is a consistent run of minor issues that add up in the same way.

- One client in the last 3-4 years has had $6,200 in specialist treatments.

- Another nearly $20,000 in claims for head injury treatment in addition to what ACC funds.

- Another $76,000 for four weeks of cancer treatment, some of that unfunded.

- The largest claim we have had that's not unfunded medicines is $265,000 for multiple surgeries for cancer in the femur. That client now has a bionic leg from the hip to below the knee.

- With around 300 claims per year coming to us, we're seeing the reality of the medical system.

Everyone is different; at the same time, we have simpler medical challenges, and it should be unsurprising that we have a limited time here too.

When we get down to it, these are not small numbers, and most New Zealand families would be hard-pressed to fund them. Your average medical policy provides $600,000 to $1,000,000 of coverage per person per year. The majority of people get nowhere near that in one year, let alone a lifetime, but it’s there if it’s needed. (Ignoring the couple of insurers that don't limit their surgery benefits)

If you take cover at 30, when most people start looking for coverage, for you and your family and hold it until age 75, as I’ve outlined, on the average premium across all providers (including UltraCare), you’ll pay about $306,649 in premiums, which is a large chunk of money. Remember, this has been over 45 years, and that’s a long time to try to save this. Without UltraCare, that average premium is $262,052. Since 2016, the average has increased by about $40,000 in total.

If you and your family have $10,000 of claims every year, which is probably unlikely but possible, you’ll have an insurance return of $450,000 straight off. If we look at average incomes over this time, it equates to around 5% of the average gross income.

- Imagine what our health system would look like if it had 5% extra funding from a direct tax. I probably wouldn't be having this chat with you, and I'd be talking about something else.

- Unfortunately, it's not going to change in a hurry; medical insurance is a significant need in society.

If you opt for the cheapest policy in this group, which is a good choice, you’ll be about $77,351 better off than the average. If you opt for the most expensive plan (UltraCare), you’ll be about $255,897 worse off than the average.

If we consider the spread on the plans excluding UltraCare, your range has reduced significantly to $3,284 more than average to $26,171 less than average. Meaning that the relatively close premium rates in your working life should not be a driver for moving providers, as the risk of exclusions is far greater than the financial benefit of lower premiums.

Interestingly, the Southern Cross Wellbeing Two plan in the middle of the pack has the fewest resources available to cover you in the future, so cheaper isn't always ideal. The cheapest plan on average is Partners Life and AIA, and both are some of the best covers on the market.

In terms of product quality, what the rating houses Quotemonster and Strategy Financial Services say, with my overlay opinion on what this translates to, in terms of order of quality, is as follows.

- Partners Life & nib (largely equally as good, and the nuances will be down to personal preference).

- Accuro now UniMed (because it is a good product, but it is not guaranteed, and they have been sold to UniMed.

- AIA solid coverage and caters to unfunded cancer medicines, whereas the ones above also cater to non-cancer unfunded medicines as well.

- Southern Cross, though the discussion on cover security with their penchant for changing benefits and general lack of support for unfunded medicines needs consideration.

- UniMed, which I have not included in the above, will change with the Accuro purchase. Historically, these policies have lagged behind the rest, but recent changes have improved their product rating.

Premium pressures and new products:

Insurers have been seeing the impact on people, with continuing rises in premiums and premature cancellations or reductions in coverage.

- This has opened the door to new benefits that are cut-down forms of some of the full-spectrum products, including coverage focused exclusively on cancer care or the big 5-6 conditions like hips, hearts, cancer, knees, and stroke.

- Sovereign's Key Health product, which was delivered back in 2005 and has since been discontinued, was ahead of its time; this sort of product today has some merit for those looking for a budget option for their medical insurance.

- A balance of either using public health or paying your own way privately for minor conditions, but having the support of insurance for the really big stuff.

- AIA have come to market with a cancer care plan that caters only to cancer treatment, and this month they have added back in the standalone Specialist and testing benefit, which helps accelerate access to the public system for surgery treatment. But still falls short against a full medical plan.

One issue that has come to light since July 2024 is how insurers are treating unfunded medicine claims; where the common understanding has been MedSafe approved, there are additional criteria with MedSafe approvals that need consideration in relation to how your insurer may or may not pay an unfunded medicines claim.

- This is a complex area I will write more about, in the meantime this article I wrote for both clinical services and the financial services industry is worth a read

I expect that we will continue to see an evolution of cover in this space as insurers juggle things to provide more strata to the present medical insurance structures.

Is Medical Insurance worth it? Definitely!

Have a chat with us about how you can do this cost-effectively so that you get the best treatment options available for your premium money and that they’re affordable for you and your family in the future.

Terms & Conditions

Subscribe

My comments